Loading blog post...

Crypto Staking Tax Treatment: What Institutions Need to Know in 2026

As 2026 marks the full implementation of the OECD’s Crypto-Asset Reporting Framework (CARF) and the EU’s DAC8, the "wait-and-see" approach to crypto staking tax is no longer viable for institutions. With tax authorities now receiving automated, block-level data, the distinction between "income at receipt" and "gain at disposal" is the most critical decision for your compliance team. This guide breaks down the structural tax implications of direct, delegated, and liquid staking for global institutions.

Institutions that stake crypto are sitting on a tax question that most jurisdictions have not fully answered yet. The assets are real, the yields are real, and the tax liability is real but the rules governing exactly when that liability arises, how it is measured, and how it is reported vary significantly depending on where you operate and how your staking arrangement is structured.

This is not a comfortable place to be for compliance teams. And 2026 is the year it is becoming impossible to ignore.

What Crypto Staking Actually Is And Why the Definition Matters for Tax

Before getting into tax treatment, it helps to define staking precisely because how a jurisdiction classifies the activity shapes everything that follows.

Crypto staking is the process of locking cryptocurrency in a blockchain network to support its consensus mechanism, in exchange for rewards. On proof-of-stake networks, validators stake the native crypto asset to participate in block production and earn yield. Delegators assign their stake coin holdings to a validator and receive a proportional share of that validator's rewards.

The tax question this creates is deceptively simple on the surface: are staking rewards income when you receive them, or when you sell them?

That question has meaningfully different answers in different jurisdictions and institutions operating across borders may face both simultaneously. Getting the classification right is not a compliance detail. It is the foundation on which every other tax calculation sits.

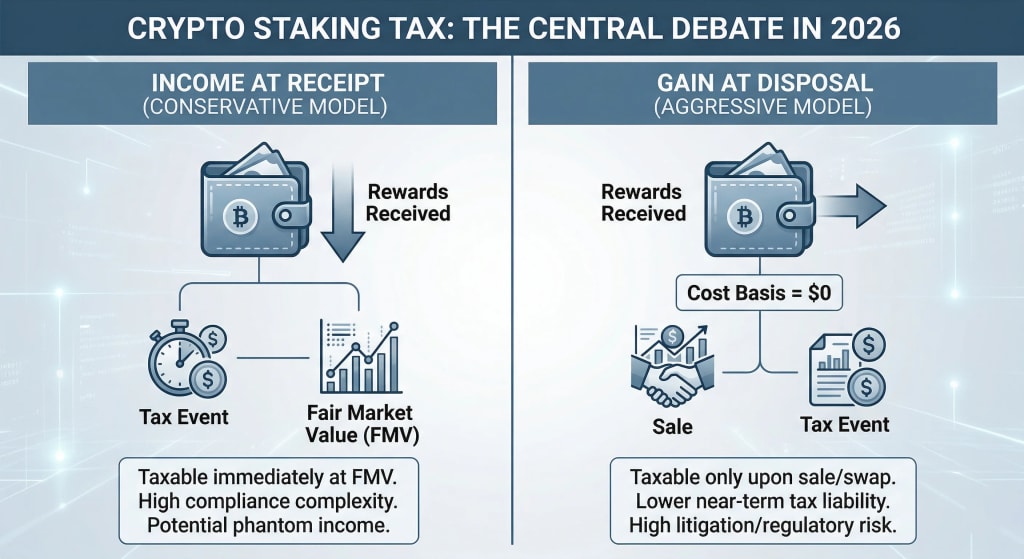

The Core Tax Question: Income at Receipt or Gain at Disposal?

This is where most institutions need to start and where the regulatory landscape is most unsettled.

- The income-at-receipt position treats staking rewards as ordinary income the moment they land in your wallet, valued at the market price at that moment. This is the position the IRS has moved toward in the United States following the 2023 guidance, and it is the more conservative approach. For institutions with large staked positions generating continuous rewards, this creates a recognition event with every epoch, potentially thousands of taxable moments per year, each requiring a market price snapshot.

- The gain-at-disposal position treats staking rewards as property acquired at zero or near-zero cost basis, with the tax event triggered only when the asset is sold. Some taxpayers argued for this position following the Jarrett case, where a couple successfully challenged IRS treatment of Tezos staking rewards as income. The IRS refunded their tax rather than litigate the case which was widely read as an acknowledgment of uncertainty rather than a concession on principle.

For institutions, the practical implication is straightforward: the income-at-receipt position creates higher near-term tax liability and significantly more reporting complexity. The gain-at-disposal position is more favorable but carries litigation risk in jurisdictions that have not explicitly endorsed it.

Most institutional tax counsel is advising clients to apply income-at-receipt conservatively, document the methodology clearly, and monitor regulatory developments closely.

How Different Staking Arrangements Change the Tax Picture

Not all staking crypto arrangements are taxed identically and the structural differences matter more than most institutions realize when they first enter the space.

- Direct validation — running your own validator node on a blockchain network is the clearest case. The institution is directly providing the staking service, the rewards flow directly to its wallet, and the income recognition question applies straightforwardly.

- Delegated staking through a third-party operator introduces a layer of complexity. If the validator operator receives rewards and distributes them after taking a commission, the question of whether the institution received the gross reward (with the commission as a deductible expense) or the net reward (with the commission already removed) affects both income recognition and basis calculation.

- Liquid staking protocols — where staking crypto through a protocol like Lido or Rocket Pool issues a derivative token (stETH, rETH) in return create a genuinely novel tax question. Is the issuance of the derivative token a taxable exchange? Does the value accrual in the derivative token constitute income as it occurs, or only at redemption? Most jurisdictions have not addressed this explicitly, and institutional tax positions on liquid staking vary considerably.

Staking through a cryptocurrency exchange introduces custodial complexity. When the institution's assets are held by the exchange and the exchange stakes on its behalf, the tax characterization may depend on whether the arrangement is treated as a lending relationship, an agency relationship, or something else entirely.

If your institution is evaluating which staking structure fits your tax and operational requirements, our Blockchain Consulting services covers the technical infrastructure behind each arrangement.

The Reporting Infrastructure Problem Nobody Talks About

Even institutions that have resolved the income-at-receipt vs. gain-at-disposal question face a second, more operational challenge: actually generating the records that tax reporting requires.

Crypto staking tax compliance at institutional scale means:

- Recording the fair market value of every reward distribution at the moment of receipt, which on Ethereum happens continuously at the consensus layer

- Tracking cost basis separately for staking rewards (received as income) versus purchased crypto (acquired through buy crypto transactions or crypto trading)

- Reconciling on-chain data with custodian records, which frequently do not match precisely due to timing differences in how rewards are recognized

- Managing unbonding periods on networks like Cosmos where unstaking takes 21 days, the illiquidity of staked assets needs to be reflected in portfolio-level reporting

The tooling for this has improved significantly. Platforms like Lukka, Ledgible, and TaxBit have built institutional-grade staking tax reporting that pulls on-chain data and applies recognition logic automatically. But the tooling is only as good as the methodology it encodes and institutions still need to make and document their own policy decisions about how rewards are classified.

Cross-Border Staking: When Multiple Tax Regimes Apply Simultaneously

For institutions operating across jurisdictions, crypto staking tax treatment is not a single question — it is a matrix of questions that intersects tax residency, source-of-income rules, and treaty positions.

A few of the practical complications worth knowing:

- The UK's HMRC has taken a relatively clear position: staking rewards are income at receipt for most institutional arrangements, subject to corporation tax or income tax depending on entity type. The clarity is welcome, even if the treatment is not favorable.

- The EU's MiCA framework harmonizes crypto asset regulation across member states but leaves significant gaps on staking tax treatment. Individual member states still set their own tax rules, meaning an institution operating across five EU jurisdictions may be applying five different recognition methodologies to the same staking activity.

- Singapore and the UAE have positioned themselves as crypto-friendly jurisdictions partly through favorable tax treatment. Singapore's IRAS has indicated that staking rewards may not constitute taxable income in certain structures — making entity structuring for staking operations a legitimate tax planning consideration for institutions with flexibility on domicile.

Withholding tax is an emerging issue as staking becomes more institutionalized. Some jurisdictions are beginning to consider whether staking rewards paid by a network to a foreign entity should be subject to withholding, a question the existing treaty infrastructure was not designed to answer.

The short version: institutions with cross-border staking operations need jurisdiction-specific advice, not a single global policy applied uniformly.

Staking vs. Mining vs. Lending: Getting the Classification Right

Crypto staking tax treatment does not exist in isolation, it sits alongside the tax treatment of crypto mining, lending, and crypto trading, and the classification of one activity affects how the others are viewed.

Cryptocurrency mining has longer regulatory history and clearer treatment in most jurisdictions: mining rewards are ordinary income at receipt, mining is treated as a trade or business for entities that conduct it at scale, and equipment costs are depreciable capital expenditures.

Where staking differs is in the passive nature of delegated arrangements. An institution that simply delegates tokens to a validator and collects rewards is arguably not conducting an active trade or business in the same way a miner is. This distinction may affect whether staking income is subject to self-employment tax in the US context, and whether it qualifies as trading income or investment income in other jurisdictions.

Crypto lending, depositing assets on a crypto exchange or lending protocol in exchange for yield is the closest structural analogue to delegated staking and often receives similar tax treatment. The key question for both is whether the yield is ordinary income or a return on investment. Getting this classification wrong creates mismatches between how income and losses from the same activity are treated.

Practical Steps Institutions Should Be Taking Now

The regulatory environment around crypto staking tax will continue to evolve. What institutions can control is the quality of their internal infrastructure and documentation. A few concrete actions worth prioritizing:

- Document your methodology now. Choose a clear, defensible position on income recognition, write it down, and apply it consistently. Inconsistent treatment across years is a red flag in any audit.

- Build on-chain data pipelines before you need them. Reconstructing reward histories retroactively from blockchain data is painful and expensive. Getting data infrastructure in place early is significantly cheaper than fixing it under audit pressure.

- Separate staking reward basis from purchased crypto basis. These are different cost basis pools with different recognition histories. Commingling them creates reporting errors that compound over time.

- Review staking arrangements structurally. Whether you stake directly, through a validator operator, through a liquid staking protocol, or through a best crypto exchange custody arrangement has meaningful tax implications. Review these before scaling, not after.

- Engage specialist counsel, not general tax advisors. Cryptocurrency tax is a specialist field. General corporate tax advisors frequently apply conventional income tax frameworks to staking in ways that produce incorrect results.

Our Web3 Regulatory Compliance Guide covers the broader compliance landscape for institutions deploying capital in blockchain technology environments. Connect today to get started.

Frequently Asked Questions

Q: When are crypto staking rewards taxable?

A: In most jurisdictions, staking crypto rewards are treated as ordinary income when received, based on market value at that time. Some argue tax applies only at disposal, but that remains higher risk.

Q: Does the type of staking arrangement affect tax treatment?

A: Yes. Direct staking, delegated staking, liquid staking, and exchange staking can each affect income classification, cost basis, and reporting differently.

Q: How is crypto staking different from crypto mining for tax purposes?

A: Cryptocurrency mining usually has clearer treatment: rewards as income and equipment as capital expenditure. Crypto staking is often treated similarly, though passive structures may change classification.

Q: What records are needed for staking tax compliance?

A: Keep reward values at receipt, cost basis records, validator fees, unbonding periods, and apply one reporting method consistently.

Q: Is crypto staking income treated differently across jurisdictions?

A: Yes. The United States, United Kingdom, European Union, Singapore, and United Arab Emirates all apply different rules, so cross-border operations need jurisdiction-specific advice.

Conclusion

Crypto staking tax treatment in 2026 remains unsettled, consequential, and increasingly difficult to ignore as major jurisdictions move toward stricter reporting standards.

The institutions handling this well are not waiting for perfect clarity. They are making defensible methodology decisions, building reporting infrastructure, and working with specialist partners such as EthElite to stay operationally prepared.

The blockchain technology behind staking crypto is sophisticated. Tax treatment is catching up and late preparation is usually more expensive.

Share with your community!