Loading blog post...

How to Unlock Real-Time Settlement in Cross-Border Payments With Blockchain

Cross-border payments are still constrained by legacy systems designed for a pre-digital era, where settlement relies on slow, message-based processes, multiple intermediaries, and fragmented ledgers. Blockchain fundamentally changes this model by unifying validation, settlement, liquidity, compliance, and FX into a single synchronized ledger. By eliminating intermediaries, reconciliation delays, and settlement risk, blockchain enables true real-time settlement with instant finality, lower costs, and full transparency. This shift doesn’t optimize existing rails, it replaces them with a programmable, global settlement engine built for modern financial infrastructure.

The world trades in real time, but money still moves like it’s stuck in a past era. Cross-border settlements crawl through layers of correspondent banks, reconciliation cycles, cut-off windows, and outdated messaging systems that were never built for the speed of modern digital markets. Businesses lose days. Banks carry unnecessary risk. Consumers pay inflated fees. The entire financial infrastructure strains under processes designed decades before the internet existed.

Blockchain changes this dynamic fundamentally. Not as a speculative asset class, but as a settlement engine engineered for global money movement. When blockchain in cross border payments becomes the underlying infrastructure, transactions no longer need middlemen to confirm, reconcile, or approve them. They finalize instantly on a shared ledger visible to every participant. Real-time settlement stops being a dream and becomes the logical outcome of a synchronized system.

Unlocking this capability requires understanding how blockchain restructures the basic mechanisms of settlement, liquidity, validation, compliance, and currency exchange across borders.

The Settlement Shift: Why Blockchain in Cross Border Payments Eliminates Legacy Delays

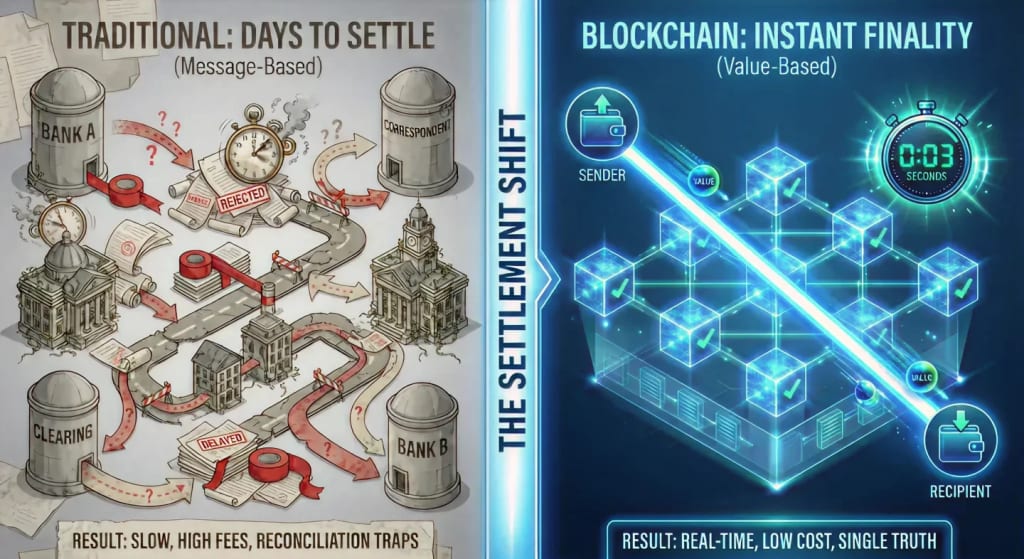

Traditional payment systems do not settle money. They settle messages. Every institution involved updates its own ledger and waits for the others to do the same. That sequential dependency creates settlement windows that stretch across hours or days. Blockchain in cross border payments replaces this fragmented architecture with a unified ledger where validation and settlement occur in one motion.

Instead of dozens of institutions confirming the same transaction in different databases, the network verifies it once through consensus. That transformation removes the friction that causes global settlements to lag, turning a multi-step relay process into a direct final update on a shared global ledger.

Teams exploring blockchain-based settlement rails can check our Blockchain Consulting services to see how this architecture is implemented in real systems.

Intermediary Collapse: How Blockchain for Cross Border Payments Cuts Out the Bottlenecks

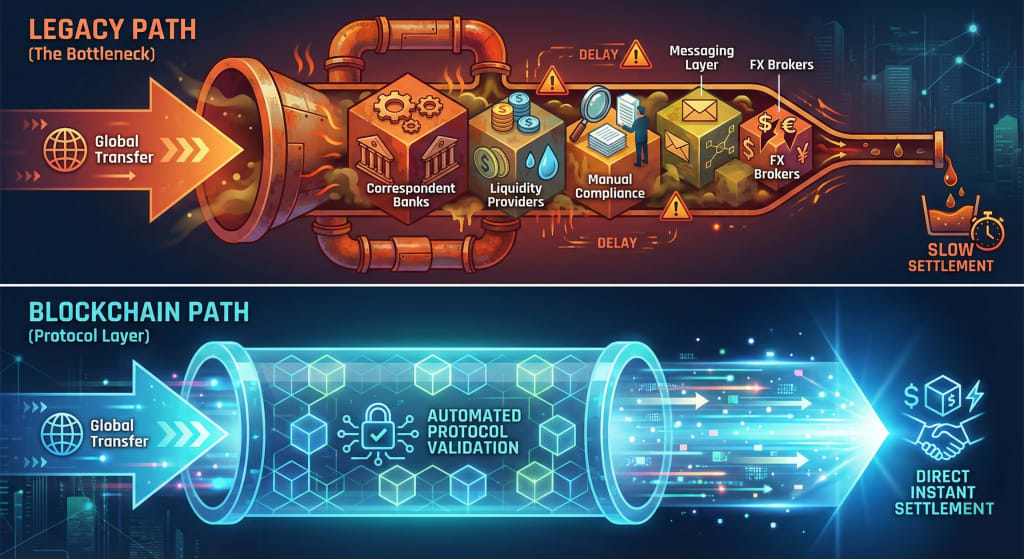

The slowest part of any international transfer is the dependency on intermediaries — correspondent banks, clearinghouses, liquidity providers, compliance processors, and messaging layers. Each one introduces delays and risk buffers, creating a chain of approval that slows down movement across time zones.

Blockchain for cross border payments compresses this entire chain by allowing the network to handle what intermediaries previously did:

- validate transactions instantly

- maintain ledger accuracy

- execute settlement directly

- eliminate multi-party approval cycles

When intermediaries disappear, delay disappears with them. Real-time settlement becomes the natural output of a system where validation is built into the protocol itself.

Shared Truth: How Cross Border Payments Blockchain Infrastructure Removes Reconciliation

The fragmentation problem in traditional finance comes from every institution maintaining its own records. Reconciliation exists only because ledgers disagree. A cross border payments blockchain ledger removes disagreement altogether. Every participant operates on a single synchronized state, meaning the instant a transaction is validated, it is final everywhere.

This eliminates daylight exposure, reduces operational risk, and removes the need for batch processing or manual ledger matching. With reconciliation collapsing into irrelevance, settlement moves at the speed of the ledger itself.

Programmable Transactions: How Blockchain Cross Border Payments Automate Compliance

Compliance is one of the biggest hidden sources of settlement delay. AML checks, sanctions screening, fraud scoring, and identity verification are often conducted in separate steps before or after the transfer. Each step introduces its own timeline.

Blockchain cross border payments streamline this by embedding compliance directly into settlement logic through smart contracts.

That means compliance becomes:

- automated, not manual

- instant, not delayed

- built-in, not bolted on

- transparent, not opaque

Instead of compliance slowing down global transfers, it becomes part of the real-time settlement pipeline.

You can see how programmable compliance is implemented in our Smart Contract Development Services.

On-Chain Liquidity: Why Blockchain in Cross Border Payments Enables Instant Value Transfer

Liquidity uncertainty is one of the most overlooked causes of slow settlement. Institutions cannot release funds until they confirm availability, leading to unnecessary holds and manual checks. Blockchain in cross border payments solves this through real-time access to balances and programmatic control of escrow conditions.

On-chain liquidity provides:

- instant visibility into available funds

- automated execution based on conditions

- no need for pre-funded accounts

- no dependency on external confirmation

When the system already knows the exact state of liquidity, there is nothing left to verify. Settlement becomes immediate.

Integrated FX: How Blockchain for Cross Border Payments Redesigns Currency Conversion

Currency conversion is usually a separate workflow, handled by different systems, using different timelines, managed by different institutions. That separation is one of the biggest reasons cross-border settlement slows down.

Blockchain for cross border payments merges FX execution into the settlement process itself. Tokenized currencies and on-chain liquidity pools allow conversion to happen in real time.

This creates:

- atomic conversion and settlement

- instant FX rate execution

- elimination of multi-day FX batching

- predictable, low-slippage transfers across currencies

When FX is integrated instead of isolated, global settlement finally becomes seamless.

Risk Eradication: How Cross Border Payments Blockchain Delivers Instant Finality

Transfers in traditional systems may appear instant, but the settlement behind them often takes days. That gap creates credit risk and forces institutions to build protection layers that slow everything down.

Cross border payments blockchain systems combine validation and finality in the same action. Once the block confirms, the transaction is immutable. There is no pending status, no clawback risk, and no reconciliation lag. Payment certainty becomes immediate.

With risk eliminated, speed becomes the natural default.

Regulatory Maturity: Why Blockchain Cross Border Payments Align With Modern Oversight

Regulation is often seen as a barrier to real-time settlement, yet blockchain cross border payments strengthen regulatory capabilities instead of weakening them. Immutable audit trails, timestamped entries, and transparent value flows let regulators monitor systems in real time rather than relying on delayed reporting.

Regulators no longer have to reconstruct transaction histories manually. The ledger provides:

- instant visibility

- verifiable audit paths

- transparent cross-border flow tracking

When regulation becomes real-time, settlement can follow without delay.

For regulated industries upgrading their infrastructure, explore our Custom dApp Development offering.

FAQ: Real-Time Settlement & Blockchain Cross-Border Payments

How does blockchain make real-time cross-border settlement possible?

By combining validation, settlement, reconciliation, compliance, and FX execution into a single synchronized ledger.

Why are blockchain transactions faster than traditional international transfers?

Traditional rails move messages; blockchain moves actual value directly on-chain without relying on multiple intermediaries.

Does blockchain help reduce the cost of cross-border payments?

Yes. Removing correspondent banks alone eliminates a significant portion of operational and transaction fees.

Is compliance slower on blockchain?

No. Smart contracts allow compliance checks to run automatically during settlement.

Can blockchain support high-volume global payments?

Modern L1s, rollups, and interoperability protocols are already handling thousands of transactions per second with instant finality.

For deeper integration guidance, Consult Now

Conclusion: The Future of Cross-Border Payments Is Already Here

The world has outgrown the limitations of legacy banking rails. Businesses operate globally, consumers transact across borders daily, and financial systems can no longer afford to wait hours or days for settlement. Blockchain doesn’t just speed up cross-border payments; it redefines the mechanics behind how money moves. When validation, liquidity, compliance, FX, and finality converge onto a single global ledger, real-time settlement becomes the logical default of a more intelligent system.

Cross-border payments blockchain infrastructure doesn’t “improve” the old model. It replaces it with a faster, cleaner, transparent, programmable alternative built for the digital economy. The shift is inevitable. The institutions that adopt it early gain the advantage of instant settlement, frictionless liquidity, and a competitive cost structure. Those who hesitate will struggle to keep pace with a world that now expects financial systems to operate at internet speed.

Real-time settlement isn’t the future.With blockchain, it’s finally the present.

Share with your community!